Big Data Analytics Market Growth Across Key End-Use Sectors

Политика и општество |

2026-01-15 09:29:14

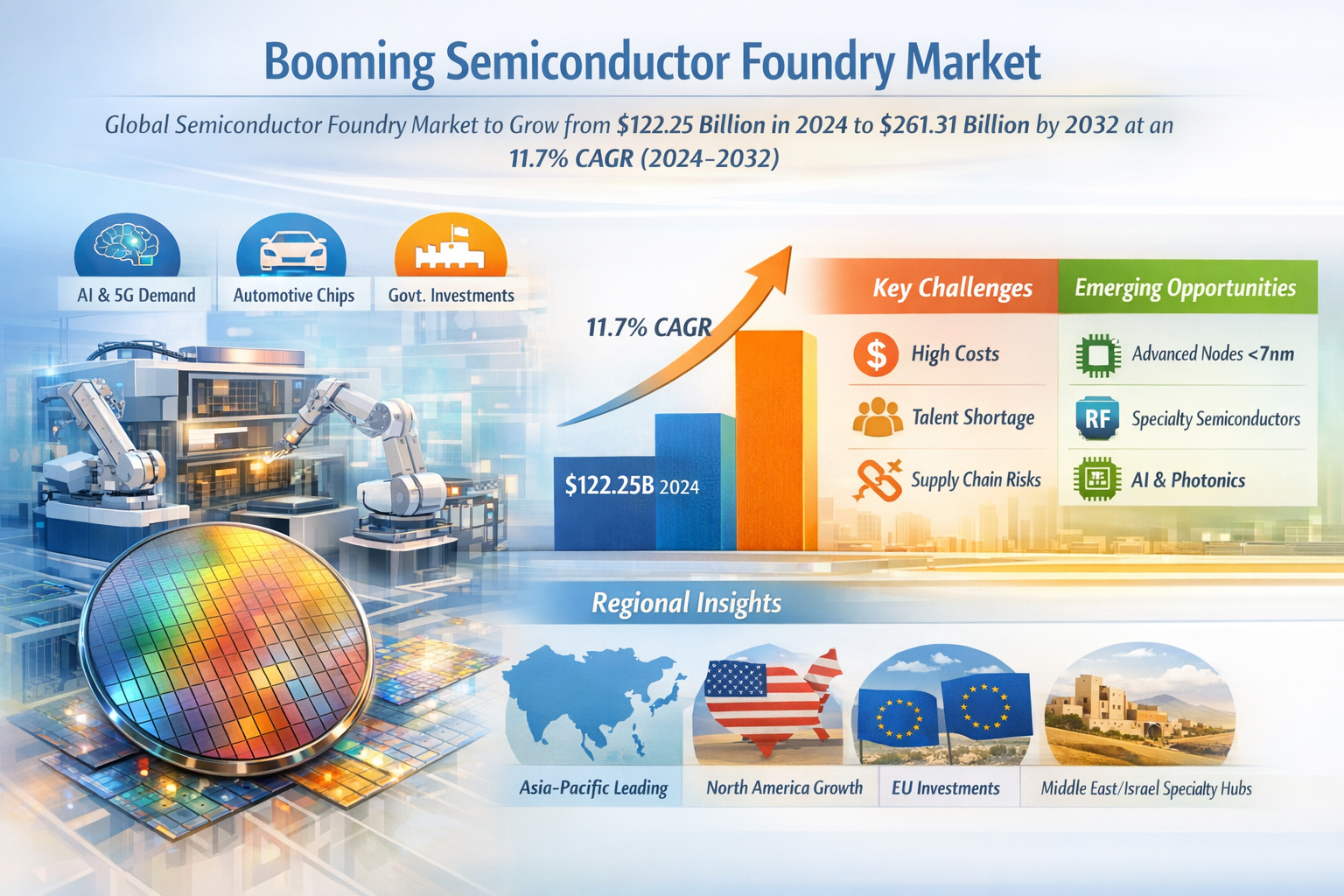

According to a new report from Intel Market Research, the global Semiconductor Foundry Service market was valued at USD 122.25 billion in 2024 and is projected to reach USD 261.31 billion by 2032, growing at an impressive CAGR of 11.7% during the forecast period (2024-2032). This substantial growth trajectory is driven by surging demand for advanced chips across multiple industries, coupled with rapid technological advancements in semiconductor manufacturing processes.

What are Semiconductor Foundry Services?

Semiconductor foundry services represent a specialized segment of the chip manufacturing ecosystem where companies focus exclusively on wafer fabrication for fabless semiconductor firms. Unlike integrated device manufacturers (IDMs) that handle both design and production, pure-play foundries provide manufacturing-as-a-service - offering advanced production capabilities without competing with their customers. This business model has become increasingly vital as semiconductor design complexity grows while fabrication costs skyrocket.

This comprehensive report provides exhaustive analysis of the global Semiconductor Foundry Service market, examining everything from macroeconomic trends to granular details about wafer sizes, process nodes, and regional dynamics. It offers actionable intelligence on competitive positioning, technological roadmaps, and strategic opportunities in this capital-intensive industry.

The research helps stakeholders understand the complex interplay between demand drivers, supply chain constraints, and technological innovation. By providing detailed market share analysis and growth projections, it enables businesses to make informed decisions about partnerships, investments, and market entry strategies.

In essence, this report is indispensable for semiconductor manufacturers, fabless chip companies, investors, policymakers, and any organization seeking to navigate the strategically critical foundry services landscape.

📥 Download Sample Report: Semiconductor Foundry Service Market - View in Detailed Research Report

Key Market Drivers

1. Exploding Demand for Advanced Process Technologies

The insatiable appetite for cutting-edge semiconductor technologies across multiple sectors represents the primary growth engine. Breakthrough applications in AI accelerators, 5G infrastructure, and autonomous vehicles require increasingly sophisticated chips manufactured at 7nm nodes and below. Foundries capable of producing these advanced components are operating at near-full capacity, with TSMC and Samsung currently dominating this high-value segment.

2. Geopolitical Reshoring of Semiconductor Manufacturing

National security concerns and supply chain vulnerabilities have prompted massive government investments in domestic semiconductor capabilities. Initiatives like the U.S. CHIPS Act and EU Chips Act are funneling billions into foundry expansion, creating new opportunities across Western markets. This strategic repositioning is reshaping global supply chains and fostering competition in what was traditionally an Asia-centric industry.

The automotive industry's rapid transformation deserves special mention. Modern vehicles now incorporate hundreds of semiconductors - from basic MCUs to advanced AI processors for autonomous driving. This vertical alone could drive 30% of foundry demand growth through 2025 as automakers increasingly turn to specialized foundries to secure supply.

Market Challenges

Emerging Opportunities

The semiconductor foundry landscape is evolving rapidly, presenting several high-potential avenues for growth:

Perhaps most significantly, the AI revolution is creating entirely new semiconductor paradigms. Foundries that can adapt to manufacture novel architectures like neuromorphic chips and silicon photonics will capture disproportionate value in coming years.

📥 Download Sample PDF: Semiconductor Foundry Service Market - View in Detailed Research Report

Regional Market Insights

Market Segmentation

By Wafer Size

By Technology Node

By Service Type

By Application

📘 Get Full Report Here: Semiconductor Foundry Service Market - View Detailed Research Report

Competitive Landscape

The foundry market remains highly concentrated, with the top five players controlling over 83% of revenue. While TSMC maintains technology leadership, intense competition is developing in specialty segments and geographic niches.

The report provides detailed competitive analysis of 15+ key players, including:

Report Deliverables

📘 Get Full Report Here: Semiconductor Foundry Service Market - View Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in semiconductors, electronics manufacturing, and emerging technologies. Our research capabilities include:

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia-Pacific: +91 9169164321

🔗 LinkedIn: Follow Us